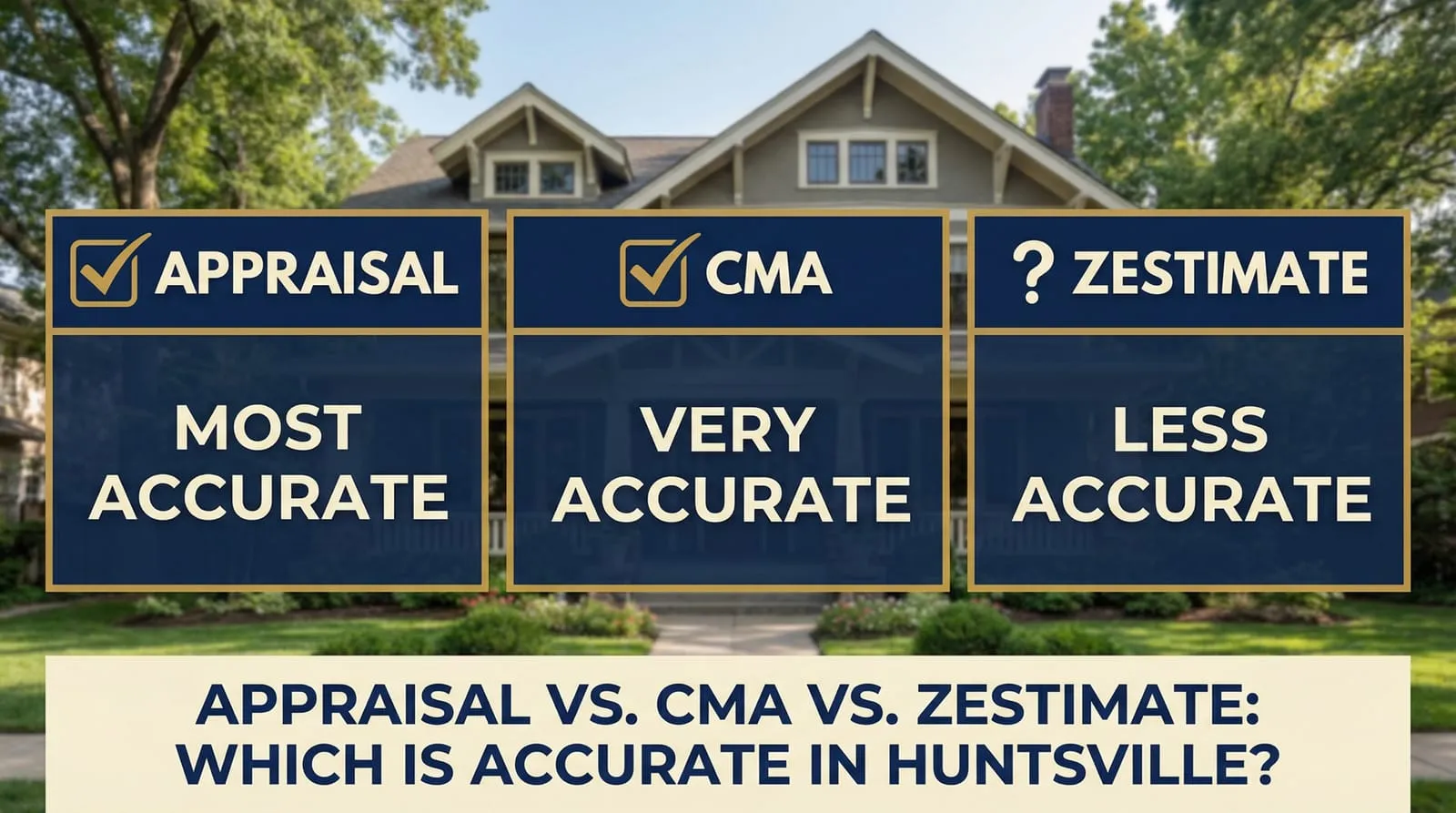

Appraisal vs. CMA vs. Zestimate: Which Is Accurate in Huntsville?

Written by Jon Smith, local Huntsville Realtor — April 2026

There are three different "values" for any Huntsville home, and they almost never match. The Zillow Zestimate says one thing. A real estate agent's CMA says something else. And when the home actually sells, the bank-ordered appraisal might come in at a third number entirely. Most Huntsville homeowners don't understand the differences between these three valuations, when each one matters, and which one to trust for which decision. Picking the wrong one for the wrong purpose can cost real money.

This is the local-Realtor breakdown of how the three Huntsville home valuations actually differ, the math behind each, where each one is most accurate, and the framework I use to know which number matters when.

Free, no obligation, based on real comps and a real local agent.

The three valuations defined

1. Zillow Zestimate (and similar AVMs) - What it is: Automated valuation generated by a machine learning model trained on millions of past sales nationally - Who produces it: Zillow's algorithm (also Redfin, Realtor.com, Chase, others) - Cost: Free - Time to produce: Seconds - Inputs: Tax assessor data, recent sales nearby, prior sale prices for the home, listing history - Doesn't see: Condition, updates, finishes, layout, lot quality, school zone precision, micro-comps - Median error rate (Zillow's own published number for off-market homes): ~6.9% in mid-sized U.S. metros — meaning half of all Zestimates are MORE wrong than that - Best for: Casual benchmarking, knowing roughly whether your home is closer to $300K or $500K - Worst for: Pricing decisions, equity decisions, financial planning

2. Real Estate Agent CMA (Comparative Market Analysis) - What it is: Professional valuation by a real estate agent based on direct knowledge of the home and recent comparable sales - Who produces it: Licensed Realtors with MLS access - Cost: Free from most Huntsville agents - Time to produce: 1–3 hours including walkthrough - Inputs: MLS data, walkthrough of the home, condition observations, sub-market expertise, adjustments for differences - Doesn't have: Legal weight (CMAs are not legally binding valuations) - Typical accuracy: Within 2–4% of eventual sale price for homes in stable sub-markets with abundant comps - Best for: Pricing strategy, equity decisions, "what's my home worth right now" decisions - Worst for: Legal proceedings, lending decisions (banks won't accept a CMA in lieu of an appraisal)

3. Bank-Ordered Appraisal - What it is: Regulated, licensed valuation produced by a state-certified appraiser - Who produces it: Independent state-licensed appraiser hired through an Appraisal Management Company (AMC) by the lender - Cost: $500–$700 typically in Huntsville, paid by the buyer at closing - Time to produce: 5–10 business days from order to delivery - Inputs: Walkthrough of the home, MLS data, public records, comparable sales analysis with required adjustments per regulatory standards - Has: Legal weight in lending and other formal contexts - Typical accuracy: Generally accurate, but with built-in conservatism — appraisers are professionally responsible for not OVERvaluing homes, so there's a structural bias toward conservative estimates - Best for: Lending decisions, refinancing, formal contexts requiring documented value - Worst for: Setting a list price (appraisals lag the market and are conservative)

When each one matters

The right valuation depends entirely on what decision you're making.

Use the Zestimate (and other AVMs) when: - You're casually curious about your home's value with no specific decision pending - You want a rough check on something the agent told you (one of multiple data points, not the determining one) - You're comparing your home to others in the same general area for relative ranking purposes - You're 2+ years away from any actual decision

Use a real agent CMA when: - You're considering selling within the next 6–12 months - You're considering tapping equity through a HELOC or home equity loan and need to know your real position - You're doing financial planning that depends on home value - You're making a buy/sell move-up or move-down decision - You're trying to decide whether your home value supports a specific financial goal - You want to verify whether an AVM number is accurate

Use a bank-ordered appraisal when: - You're refinancing your mortgage (the lender requires it) - You're buying or selling a home (the buyer's lender will order one) - You need a legally documented value for a formal proceeding (estate, divorce, tax matter — though these may use a different appraisal type) - You're in a contract dispute that requires a third-party value

The mistake most Huntsville homeowners make: using the Zestimate for decisions that should require a CMA, or expecting a CMA to substitute for a required appraisal. Both errors cost money.

How the three valuations compare in practice

For any given Huntsville home, the three values typically rank in a predictable pattern depending on the market and the home's characteristics:

In a rising market: Zestimate < CMA ≈ Appraisal (the Zestimate lags; the CMA is current; the appraisal is current but conservative)

In a flat market: Zestimate ≈ CMA ≈ Appraisal (all roughly aligned, with random variation)

In a falling market: Zestimate > CMA > Appraisal (the Zestimate lags down; the CMA is current; the appraisal is conservative on the way down)

For homes with significant updates the algorithm doesn't know about: Zestimate < CMA ≈ Appraisal (the Zestimate misses the updates; the CMA and appraisal both see them in person)

For homes with significant deferred maintenance: Zestimate > CMA ≈ Appraisal (the Zestimate doesn't see the maintenance issues; the CMA and appraisal both do)

For unusual or one-of-a-kind properties: All three diverge substantially. The Zestimate is essentially useless. The CMA depends heavily on the agent's experience with similar properties. The appraisal can vary widely depending on the appraiser's approach.

A real client story

Late 2025 a homeowner in Madison City asked me to look at her home before refinancing. Her Zestimate at the time: $402,000. She and her husband were planning to refinance to free up some cash and were going to base the cash-out amount on the Zestimate.

I walked the home and produced a CMA. The home had been updated extensively (kitchen 2022, both bathrooms 2023, new HVAC 2024). It was in the Bob Jones zone in a tight sub-market. My CMA range: $445,000 to $458,000.

That's a $43K–$56K gap above the Zestimate. They were leaving meaningful equity on the table.

The refinance went forward. The bank-ordered appraisal came in at $452,000 — squarely in my CMA range. They were able to cash out $30K more than they would have based on the Zestimate.

Her takeaway after closing: "If we'd used the Zestimate to plan the refinance, we'd have asked for $30K less — meaning the bank would have approved $30K less, meaning we'd have walked away with $30K less. The Zestimate cost was just $0 in fees and $30K in opportunity."

A different client, same period, opposite outcome. A Hampton Cove homeowner in the $625K range. Zestimate: $645,000. He listed at $649,000 based on the Zestimate plus a small premium. Listed for 110 days. Two price reductions. Final sale: $612,000.

I had warned him in advance, in a CMA: $610,000 to $625,000 was the realistic range for his sub-market and price band. The $645K Zestimate was the algorithm not knowing how soft the $625K+ Hampton Cove price band had become in the rate environment. He decided to trust the Zestimate over the CMA.

His take after closing: "I should have listened to the agent who walked through the house. The Zestimate was telling me what I wanted to hear. The CMA was telling me what I needed to hear."

Two clients, same issue, very different outcomes. The lesson: the Zestimate is a free tool with a real error rate. The CMA is a free professional valuation with much lower error rate. The decision about which to trust should be based on the consequences of being wrong, not on which is more convenient.

Original Jon insight: the "appraisal anchoring" problem few Huntsville sellers see coming

Here's something that affects almost every Huntsville sale and which most sellers don't fully understand: the appraisal that comes in during your sale doesn't just affect the financing of that one transaction — it becomes a comp in the algorithm and affects every Zestimate within a half mile for the next 12 months.

The mechanics:

- You sell your home for $415K. Cash, appraisal, contract — done.

- The appraisal at $415K confirms the price.

- The closed sale enters MLS and public records.

- Within 30–60 days, every AVM in the country processes that closed sale.

- Your sale becomes a "comp" for every nearby home in the algorithm's analysis.

- Your neighbors' Zestimates adjust based on your sale price.

This means YOUR sale price is shaping THEIR equity calculations. If you sold for $415K when the home was actually worth $430K, you didn't just leave $15K on your own table — you pulled DOWN every Zestimate in your neighborhood for the next year. Your neighbors who use those Zestimates to guide their own decisions are now using a number that's been pushed down by your underpriced sale.

The corollary: the Zestimate is a measurement of past sales, not present values. Each transaction is a vote that pulls the Zestimate average in one direction. If a neighborhood has a series of well-priced sales, the Zestimates rise. If a neighborhood has a series of underpriced sales (because sellers anchored on low Zestimates and listed too cheap), the Zestimates spiral down.

The implication for individual sellers: don't anchor your list price on the Zestimate, because the Zestimate may have been pulled DOWN by neighbors who anchored on low Zestimates before you. Use a real CMA. Set a real market price. Sell well. Your sale will then be a "vote" that pulls the Zestimates in your area in a direction that reflects actual market value, not in a self-reinforcing cycle of underpricing.

The implication for refinancers: if you're refinancing and you need the appraisal to come in at a certain number, the most important thing you can do is have a real CMA in hand BEFORE the appraisal is ordered. A good CMA gives you the comps the appraiser should use. An honest agent will share those comps with the appraiser at the inspection, which is allowed and which often makes the appraisal more accurate. Without that input, the appraiser may default to comps that are easier to find but less representative of your home's true value.

Most Huntsville homeowners think the appraisal is an independent, mechanical process. It is independent in the sense that the appraiser is hired through an AMC and isn't allowed to talk to the lender or the borrower in ways that compromise objectivity. But it is NOT mechanical — the appraiser still has to choose which comps to use, what adjustments to apply, and how to weigh different inputs. Giving the appraiser good information is allowed, useful, and routinely changes appraisal outcomes by 3–7%. I have walked dozens of Huntsville refinances through this process. The ones where the agent provides a real CMA and supporting comps to the appraiser at inspection regularly come in higher than the ones where the appraiser is left to find their own data.

Use the right tool for the right job. Stop trusting the Zestimate for decisions that require real analysis. Get a real CMA. And if you're going through a formal appraisal, give the appraiser the data they need to come up with the right number.

Frequently Asked Questions

Which is more accurate, Zestimate or CMA? A CMA from a quality local Realtor is significantly more accurate than the Zestimate for almost every Huntsville home. The Zestimate has structural blind spots that a CMA addresses.

Will the appraisal match my CMA? Often yes, especially for stable homes in sub-markets with abundant comp data. They use similar methodology. Differences usually come from the appraiser's choice of comps or adjustments. Significant differences (5%+) are worth investigating.

Can I challenge a low appraisal? Yes, through a "Reconsideration of Value" (ROV) process. You can submit additional comps or evidence that the appraisal missed. Success rates vary; about 10–20% of ROVs result in a value adjustment.

Do all lenders use the same appraisal? For a single transaction, the lender orders one appraisal. If the loan changes (e.g., you switch lenders mid-transaction), a new appraisal may be required.

Is the Zestimate ever right? Sometimes — for stable, average homes in established sub-markets with abundant recent sales, the Zestimate is often within 5% of true value. For unusual homes, updated homes, or fast-moving sub-markets, it's frequently off by 10%+ in either direction.

Do appraisers use the Zestimate? No. Professional appraisers are trained to use MLS data and other primary sources, not consumer-facing AVMs.

How much does an appraisal cost in Huntsville? Typically $500–$700 for a standard residential appraisal. Higher for unusual properties or rural locations.

Next step

The right valuation tool for your Huntsville home depends on the decision you're making. For most decisions (selling, equity, financial planning), you need a real CMA — not a Zestimate, and not a future appraisal you don't have yet.

Real CMA, real local insight. Free, no obligation.

Related reading:

- How Home Valuations Actually Work in Huntsville (Beyond Zillow)

- Why Your Zillow Zestimate Is Wrong in Huntsville

- How a CMA Works: What Huntsville Agents Actually Look At

- Should I Sell My Huntsville Home Now or Wait?

- Home Appreciation by Neighborhood: Huntsville 5-Year Report

Jon Smith is a licensed Alabama Realtor serving Huntsville, Madison, Hampton Cove, Owens Cross Roads, and the broader Madison County area. CMAs are not appraisals; for legally binding valuations, consult a licensed appraiser. This guide reflects April 2026 conditions.